Where do Dubai businesses usually find savings?

Rent at renewal, licence and subscription consolidation, banking and FX charges, insurance retendering, and the long tail of unowned recurring spend — typically 5-15% of the base.

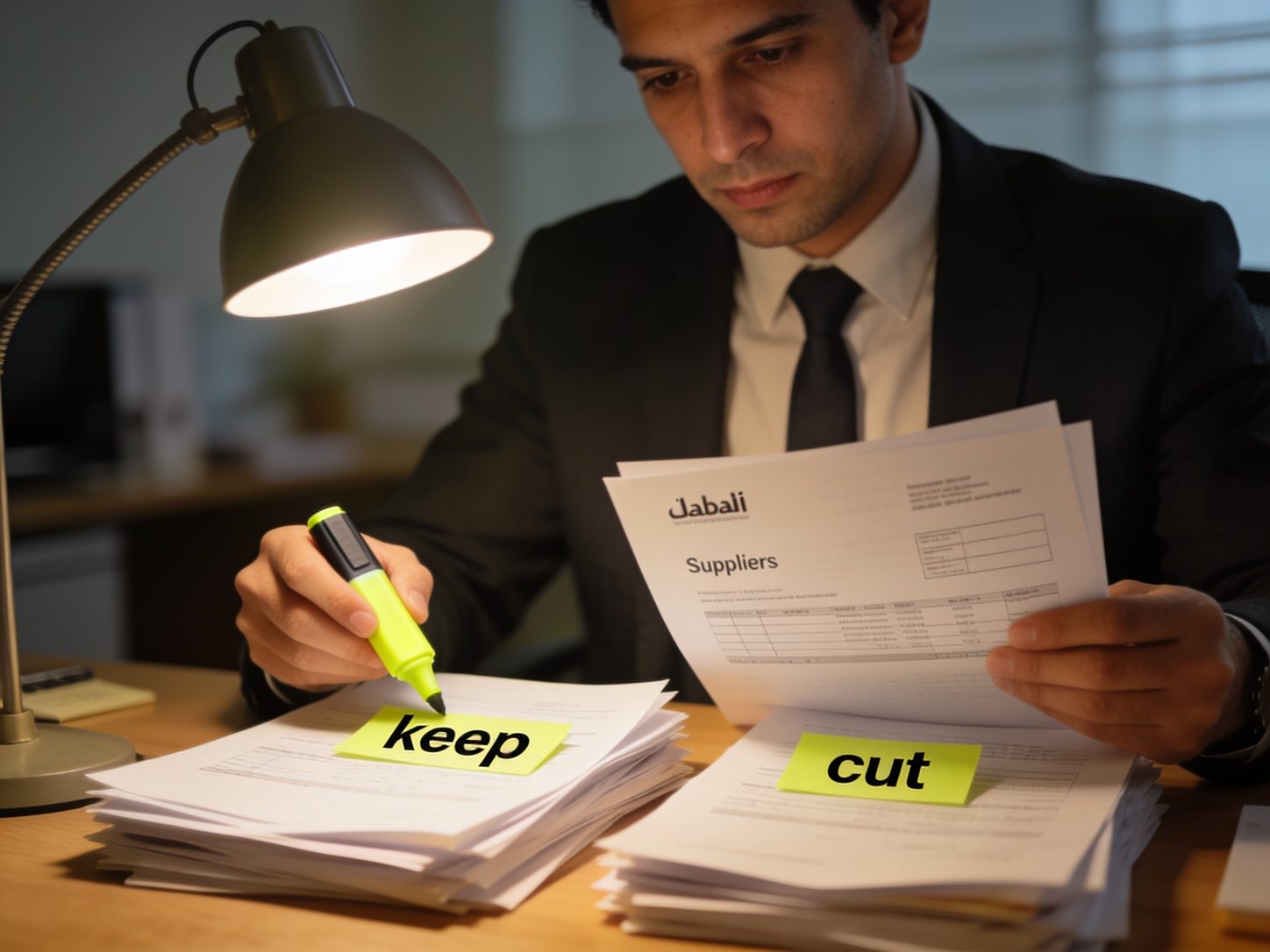

Cost Control

Costs creep in Dubai the way they creep everywhere — renewals auto-approved, subscriptions orphaned, headcount added in good months — plus local specifics: rent cheques, visa cycles, licence stacks. Cost control is the discipline of knowing which dirhams buy results and which buy habit.

Dubai-based management accounting for decision-ready numbers.

Effective cost control runs in three passes: analysis (twelve months of spend categorised and ranked — the top 20 vendors usually cover 80%), action (renegotiate, consolidate or eliminate line by line, including UAE levers like rent renegotiation, licence consolidation and visa timing), and control (approval thresholds, budget ownership and renewal calendars so the creep doesn't return). Margin analysis by product and client runs alongside — some costs should grow.

Cost-cutting without analysis amputates at random. The first pass is boring and decisive: every dirham of twelve months' spend, categorised, ranked by vendor and type, tagged by contract status. The pattern is always the same — a top-20 list that dominates, a long tail of subscriptions and small vendors nobody owns, and a few categories priced years ago.

Local cost structures have local levers. Office rent is negotiable at renewal in most market conditions — and hybrid work shrank many space needs. Licence stacks accumulate across zones and activities that consolidation can thin. Visa and manpower costs respond to nationality mix, timing and outsourced-vs-sponsored decisions. Bank charges and FX spreads yield to a single afternoon of comparison.

Not all cost is bad and not all revenue is good. Allocating real costs to products, clients and channels routinely reveals loss-making bestsellers and quiet high-margin lines — the analysis that redirects effort rather than just trimming it. The follow-through is controls: approval limits, budget owners, and a renewal calendar that forces a decision before every auto-renewal.

Rent at renewal, licence and subscription consolidation, banking and FX charges, insurance retendering, and the long tail of unowned recurring spend — typically 5-15% of the base.

Blanket cuts hit muscle and fat equally. Analysis-led control cuts specific lines for specific reasons — and grows the costs that carry high-margin work.

Allocating true costs (including service time and payment delays) to each client relationship — which usually reveals that a familiar 'big client' is barely profitable.

Controls: approval thresholds, named budget owners and a renewal calendar. Without them, the creep returns within two budget cycles.

Three to five weeks for analysis and the action plan on a typical SME spend base; implementation runs with your team over the following quarter.

Twelve months of data, three weeks of analysis, and you will know which dirhams work for you — and which just renew themselves.